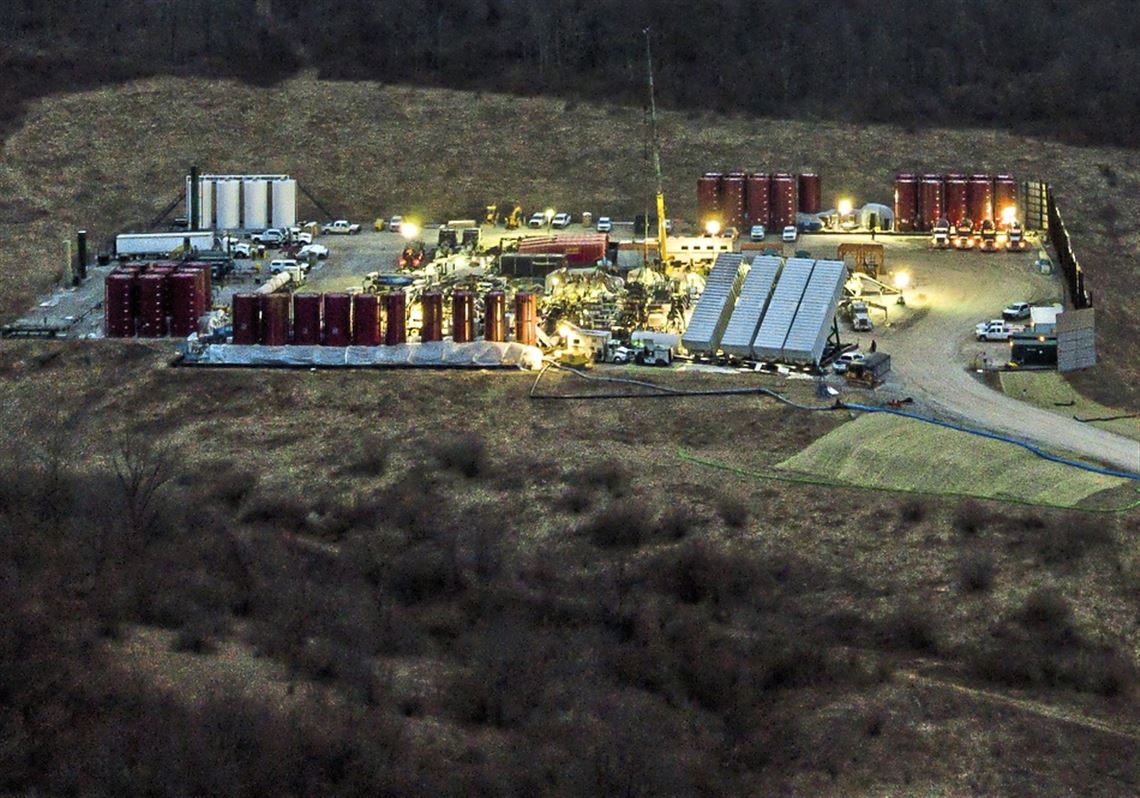

WASHINGTON — For the last decade, drilling rigs dotting the Western Pennsylvania landscape unlocked vast natural gas reserves trapped by the Marcellus Shale rock formation — and were financed with cheap corporate loans repaid at rock-bottom interest rates set by the Federal Reserve.

Now, in the midst of a global pandemic that has caused energy prices to plummet, the natural gas industry — joined by House Republicans from Pennsylvania — are asking the Federal Reserve to help them make those loan payments.

The industry has flooded the Fed and U.S. Treasury Department with letters in recent days seeking to use a new small-business government loan program to service other outstanding loans. The Fed, under rules for the Main Street Lending Program released April 9, has prohibited smaller companies from using those loans to pay off existing debt. But the central bank could modify the program based on more than 2,000 public comments it received about the program.

“Oil and natural gas producers are not looking for a government handout; they are seeking a bridge to help survive this economic disruption,” wrote Barry Russell, president and CEO of the Independent Petroleum Association of America.

Providing loans to “pay off outstanding debts coming due before this crisis subsides will be the bridge to recovery for businesses that would have otherwise been able to meet their debt obligations, were it not for the virus,” Mr. Russell wrote.

The debate highlights the challenge faced by federal officials as they quickly craft loan programs that, ideally, funnel assistance to the businesses most in need and most essential to stave off economic collapse.

The question of loan eligibility is particularly difficult for small-business loan programs, as the definition of a “small business” can range from coffee shop with a handful of employees to capital-intensive companies in the energy sector.

A separate Main Street loan program — the Paycheck Protection Program run by the Small Business Administration — was depleted in a couple of weeks by a range of companies, including large restaurant and hotel chains. That spurred criticism that many mom-and-pop shops were crowded out by large hospitality companies with franchised locations that individually counted as small businesses.

The Fed also is confronting the possibility of issuing loans to help bail out companies that took on too much risky debt in recent years — in part because of the Fed’s own monetary policies.

Following the 2008 financial crisis, the Fed kept its benchmark interest rate near zero, before slowly raising it above 2% in 2018. Under constant public criticism from President Donald Trump, the Fed began gradually lowering the rate once again.

On March 15, in response to the pandemic, the Fed slashed the rate to a range of 0% to 0.25%.

The low interest rates spurred companies to take on cheap loans to finance capital projects, acquisitions and operations. Total U.S. corporate debt soared to record high of $10 trillion in December.

Pittsburgh companies have drawn credit to make acquisitions. Wabtec Corp., the Pittsburgh-based manufacturer of rail products that recently merged with GE Transportation, reported total debt of $4.4 billion at the end of 2019, more than six times its debt load in 2015.

U.S. Steel, which bought a stake in an Arkansas steel company last year, reported debt of $3.6 billion at the end of 2019, up from $2.4 billion the prior year.

Natural gas companies commonly rely on debt as a tool to finance exploration and production, said Kathryn Miller, president of BTU Analytics. A gas well can produce for 20 to 50 years, providing collateral on those loans, she said.

Yet debt can be “a dangerous tool at times, especially in a commodity market where prices are beyond your control,” Ms. Miller said. “Markets were already difficult to refinance before we came into this global pandemic, and now credit markets are exceedingly difficult.”

“You’ve really got producers in a tough spot right now,” she said, adding that they are trying to find enough cash to keep daily operations running while making necessary payments and refinancing. She noted that part of the cycle of their business is that they have to refinance the debt that’s in their capital structure.

Range Resources Corp., a Fort Worth, Texas-based natural gas driller, highlighted that situation to federal officials. A majority of its 649 employees are in the Pittsburgh region, where the company has been “a distinctly American success story,” said Jeffrey L. Ventura, the company’s president and CEO.

“Many small businesses, like Range, are seeking a bridge from crisis to recovery,” Mr. Ventura wrote in an April 16 letter.

“Disruptions to economic activity have heightened the need for companies to obtain financing in order to pay off existing short- and near-term debt maturities,” he wrote.

Range Resources’ debt stood at about $3.2 billion at the end of 2019, down from $3.8 billion the year before. A spokesperson for the company did not reply to a request for comment.

Some lawmakers have pushed the Fed to raise the maximum loan of $25 million.

“Natural gas producers’ cash flows and costs are much higher than those of an average company,” stated a letter signed by a dozen Republican House members, including Rep. Guy Reschenthaler, R-Peters, and Rep. Mike Kelly, R-Butler. “Demand for natural gas has cratered, and the debt market is all but closed.”

Another view

Some within the oil and gas industry have a different view.

Scott Sheffield, CEO of Pioneer Natural Resources, told Texas regulators earlier this month that producers had taken too many risks borrowing money to expand operations.

“No one wants to give us capital because we have all destroyed capital and created economic waste,” Mr. Sheffield said.

And CNX Resources, a Cecil-based natural gas producer, said in statement Tuesday it will not be asking for a Main Street program loan. CNX reported $2.8 billion in debt on Dec. 31.

“We’ve previously laid out our plans to continue to service debt through organic cash flows,” said Brian Aiello, spokesman for CNX, in a written statement Tuesday. In natural gas exploration and production, he said “you have to be prepared to successfully weather down cycles and make decisions that put you in that position, and that’s what we’ve done.”

And some banking industry groups filed objections to the Fed’s initial rules that, they said, excludes many small businesses that have smaller balance sheets.

The Fed defines smaller businesses as having 10,000 employees or fewer or 2019 revenues of $2.5 billion or less. The minimum loan is $1 million.

“The minimum loan amount should be no higher than $100,000,” wrote Rebeca Rainey, president and CEO of the Independent Community Bankers of America. “Otherwise, Main Street businesses and community banks will not participate.”

With the Paycheck Protection Program out of funds, she added, “it is critical that the Federal Reserve turn its attention to making the Main Street Lending Program more attractive to both community banks and small businesses.”

Daniel Moore: dmoore@post-gazette.com, Twitter @PGdanielmoore.

First Published: April 22, 2020, 10:00 a.m.